Banks and the Magic of Finance Class 7 Question Answer SST Part 2 Chapter 8

Banks and the Magic of Finance Class 7 Questions and Answers

Class 7 SST Part 2 Chapter 8 Question Answer

The Big Questions (Page 193)

Question 1.

What is financial infrastructure, and what does it comprise?

Answer:

Financial infrastructure helps in the smooth flow of money in the economy. It includes banks, post offices, ATMs, digital payment systems and stock markets. It also includes institutions like the Reserve Bank of India (RBI). These systems help people save, borrow and transfer money safely. Financial infrastructure supports trade and daily economic activities.

Question 2.

What are the main functions performed by banks and how do they impact people’s lives?

Answer:

- Banks accept deposits and keep money safe.

- They give loans to people, farmers and businesses.

- Banks provide payment services like ATM, UPI and cheques.

Banks impact people’s daily lives. They help people to save money and earn interest. Banks help businesses by giving loans for starting their work. Banks make daily life easier, safer and more organised.

Class 7 Social Science Part 2 Chapter 8 Question Answer

Question 3.

How does financial infrastructure contribute to a nation’s progress?

Answer:

(a) It helps in mobilising savings for investment.

(b) It supports businesses, industries and agriculture.

(c) It promotes digital and cashless transactions.

(d) It creates employment opportunities.

(e) Strong financial infrastructure leads to economic growth and development.

Let’1 Explore

Question 1.

This picture is from a bank. What do you think the people are doing? Ask your family members if they have visited a bank and learn more about the activities there. (Page 194)

Answer:

People in banks handle money for individuals and businesses, focusing on customer service (opening accounts, processing transactions, solving problems), sales (offering loans, credit cards, investments), and financial management (analyzing loans, managing accounts, advising on investments), all while ensuring security and compliance.

Yes, my all family members have visited the bank. Banks provides us many facilities like our valueables are safe in banks, offers guidance on savings, investments, retirement planning, and managing wealth and offer self-service options like ATMs or digital kiosks for quick transactions.

Think About It

Question 1.

Why does Navdeep think that saving at the bank is better than keeping cash at home? (Page 196)

Answer:

Navdeep thinks that saving money at the bank is better than keeping cash at home primarily for reasons of safety, earning potential, and better financial management.

Question 2.

Can Navdeep and Rima lend to each other directly without the bank? What could happen in that case? Discuss. (Page 196)

Answer:

Yes, Navdeep and Rima can lend money to each other directly without involving a bank. This is a common practice known as peer- to-peer (P2P) lending or informal lending between individuals. After discussion we have both positive aspects and risk problems too.

Positive aspects:

- By cutting out the bank, they avoid bank fees and potentially benefit from better interest rates than those offered by traditional financial institutions.

- Successfully managing a direct loan can build trust and strengthen their personal relationship if handled responsibly

Risk factors:

- The biggest risk is the potential for the loan to cause a strain on their personal relationship. Disagreements over repayment, late payments, or a default can lead to conflict

- If Navdeep defaults, Rima bears the entire financial loss directly, with no government or institutional insurance (like deposit insurance) to fall back on.

- Depending on the jurisdiction and the amount of interest charged, there might be tax implications for Rima as the lender(interest income) or for Navdeep in certain scenarios, which they would need to manage without bank guidance.

Question 3.

How does one track so many transactions of deposits and withdrawals? (Page 198)

Answer:

The bank provides the account holder passbook that records every deposit and withdrawal. By checking the passbook regularly, a person can easily keep track of all their financial transactions. Nowadays it is also available online.

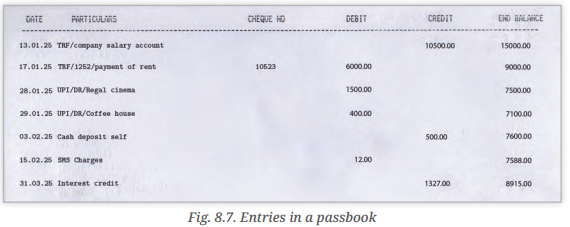

Question 4.

Look at the passbook in Fig. Observe all the particulars under the expenses (debit) and income (credit). Why is keeping records of financial transactions important? Discuss in the class. (Page 198)

Answer:

Keeping a passbook is crucial for a tangible record of all your bank transactions (deposits, withdrawals, transfers, interest) providing easy tracking, verification against bank statements, security against cyber threats, and documentation for loans or financial planning, ensuring you have a reliable, paper-based history of your finances even without digital access.

Question 5.

Why do companies issue shares, and why do people buy them? Are there any benefits of owning shares? (Page 209)

Answer:

Companies issue shares primarily to raise capital for growth, operations, or acquisitions, while people buy them to generate personal wealth through potential appreciation and dividends. Owning shares provides several benefits, including ownership rights, potential for capital gains, and income through dividends.

Class 7 Banks and the Magic of Finance Question Answer

Questions and Activities (Page 211-212)

Question 1.

What is financial infrastructure? How does it complement physical infrastructure?

Answer:

Financial infrastructure is the system that helps in the flow of money. It includes banks, ATMs, UPI, post offices, stock markets, and RBI. It complement as it physical infrastructure because as roads and railways help people moving from one place to another, like this financial infrastrusture helps money move quickly and safely among people, businesses and the government.

Question 2.

How does having a bank account help people? Should everyone be required to have a bank account?

Answer:

A bank account keeps money safe and secure, helps people to save money and earn interest. It allows easy payments through ATM. UPI, and cheques. Government benefits are sent directly to bank accounts.

Yes, everyone should have a bank account for financial inclusion.

Question 3.

What could be the possible advantages and disadvantages of compound interest for savers and borrowers?

Answer:

Advantages

- Savers earn interest on interest.

- Money grows faster over time. Disadvantages

- Borrowers have to pay more money.

- Interest amount keeps increasing, making the loan costlier.

Question 4.

How does financial infrastructure enable the flow of money between households and businesses? Can you think of how the government can facilitate this flow?

Answer:

Financial infrastructure enables money to flow by allowing households to save money in banks. Which then lend this money to businesses and industries. The government supports this through digital payments, RBI rules, and banking schemes. This keeps the economy moving smoothly.

Question 5.

What could be the reason for the higher interest rate earned on fixed deposits as compared to a savings account?

Answer:

Fixed deposits can higher interest because money in fixed deposits is locked for a fixed time and cannot withdrawn immediately. Banks can use this money for long-term loans and savings accounts allow frequent withdrawals. Hence, fixed deposits give higher interest.

Question 6.

Sahil received ₹10,000 as a prize in a poster-making competition. His father promises to pay him 12 per cent interest per year if he does not spend the amount. After 3 years, how much money would Sahil have?

Answer:

Sahil received ₹ 10,000 as a prize. His father promised to give him 12% interest per year if he does not spend the money.

If it is simple interest: Each year, Sahil will earn 12% of ₹ 10,000, which is ₹ 1,200. Over 3 years, he will earn ₹ 1,200 × 3 = ₹ 3,600 as interest. Adding this to his original ₹ 10,000, he will have a total of ₹ 13,600 after 3 years.

If it is compound interest: With compound interest, the interest earned each year is added to the total amount, so the next year’s interest is calculated on a slightly larger amount. After 3 years of adding interest in this way, Sahil will have

Year 1: 10,000 + 12% = ₹11,200

Year 2: 11,200 + 12% = ₹12,544

Year 3: 12,544 + 12% = ₹14,049 (approx.)

Sahil will have about ₹14,049 after 3 years.

Question 7.

How does the stock market help mobilise the savings of individuals? In what ways do companies benefit by issuing shares to people?

Answer:

- People invest savings by buying shares.

- Companies get money for expansion and growth.

- Investors may earn dividends and profits.

- Companies do not need to repay shares like loans.

- This helps both people and businesses.

Question 8.

How can we balance the convenience of digital payments with the risk of cyber fraud?

Answer:

We can balance the convenience of digital payments with the risk of cyber fraud. By using strong passwords and PINs. Never share OTP or bank details. Use trusted apps only. Report fraud immediately on 1930 or cybercrime.gov.in. Awareness helps enjoy convenience safely.

Question 9.

Ask your family members or neighbours about—

Question (i).

how they save money?

Answer:

- Most family members save money in bank savings accounts.

- Some also invest in fixed deposits and post office savings schemes.

- Saving in banks is preferred because it is safe and earns interest.

Question (ii).

whether they use UPI, ATM or cheques, the kinds of transactions they perform through UPI; do they find UPI better than using cash or not, and why.

Answer:

- Family members commonly use UPI and ATM cards.

- UPI is mainly used for paying bills, shopping, and sending money.

- Cheques are used for school fees and utility payments.

- Most people find UPI better than cash because it is fast, easy, and does not require carrying money.

Question (iii).

if they or their acquaintance have experienced digital fraud, for instance, through a fake call or message asking for bank details. What did they do when they realised it was a scam, and what did they learn from that experience?

Answer:

- One neighbour received a fake call asking for OTP and bank details.

- They realised it was a scam and ended the call immediately.

- They informed the bank and did not share any information.

- They learned never to share OTPs or personal details and to report fraud quickly.

Question (iv).

Summarise your findings in a table or short report. Share one surprising insight with your class.

Answer:

Survey Report (Sample Answer)

Summary Table

Aspect | Observation |

Savings method | Bank accounts, fixed deposits |

Payment modes | UPI, ATM, Cheques |

UPI use | Bill payments, shopping |

Digital fraud | Fake calls asking for OTP |

Action taken | Call ended, bank informed |

Surprising insight:

Many people find UPI faster and safer than cash, but only when used carefully.

Question 10.

Create a Financial Safety Poster.

- Design a poster with dos and don’ts of digital banking safety (for example, not sharing OTPs, reporting frauds).

Answer:

Students, Do it yourself some hints.

DOs

- Keep PINs and passwords secret

- Use official apps only

- Check messages before clicking

DON’Ts

- Do not share OTP

- Do not trust unknown calls

- Include emergency numbers or websites like https://cybercrime.gov.in or 1930 helpline.

- Hang the posters in school corridors or the library.

Website: cybercrime.gov.in

Question 11.

Cheques are often used to pay utility bills. Ask your parents to allow you to fill out the cheques for a few monthly payments.

Answer:

Fill a few sample cheques under the guidance of a parent.

Activity: Filling a Cheque (Learning Task)

- Write the date clearly.

- Write the payee’s name correctly.

- Write the amount in numbers and words.

- Sign neatly in the signature box.

- Cross the cheque for safety.

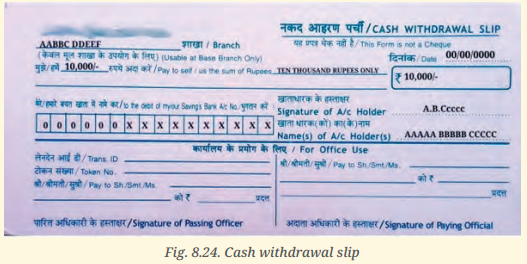

Question 12.

Suppose you have to withdraw ₹ 10,000 from your bank account, how would you fill out the cash withdrawal slip at your bank? Let us try below!

Answer:

Observe the sample withdrawal slip and fill the details.

To fill a cash withdrawal slip, I would write my name, account number, date and the amount I want to withdraw, which is ₹ 10,000. I would also write the amount in words, sign the slip and attach it with my passbook before giving it to the bank cashier. The cashier would verify my details and then pay the amount in cash to me.

Exploring Society India and Beyond Class 7 Solutions

More from Class 7

- Banks and the Magic of Finance Class 7 Extra Questions and Answers SST Part 2 Chapter 8

- Infrastructure: Engine of India’s Development Class 7 Extra Questions and Answers SST Part 2 Chapter 7

- The State, the Government, and You Class 7 Extra Questions and Answers SST Part 2 Chapter 6

- India, a Home to Many Class 7 Extra Questions and Answers SST Part 2 Chapter 5

- Turning Tides: 11th and 12th Centuries Class 7 Extra Questions and Answers SST Part 2 Chapter 4

- Empires and Kingdoms: 6th to 10th Centuries Class 7 Extra Questions and Answers SST Part 2 Chapter 3

More in Social Science

- Banks and the Magic of Finance Class 7 Extra Questions and Answers SST Part 2 Chapter 8

- Infrastructure: Engine of India’s Development Class 7 Extra Questions and Answers SST Part 2 Chapter 7

- The State, the Government, and You Class 7 Extra Questions and Answers SST Part 2 Chapter 6

- India, a Home to Many Class 7 Extra Questions and Answers SST Part 2 Chapter 5

- Turning Tides: 11th and 12th Centuries Class 7 Extra Questions and Answers SST Part 2 Chapter 4

- Empires and Kingdoms: 6th to 10th Centuries Class 7 Extra Questions and Answers SST Part 2 Chapter 3